SMM, January 19:

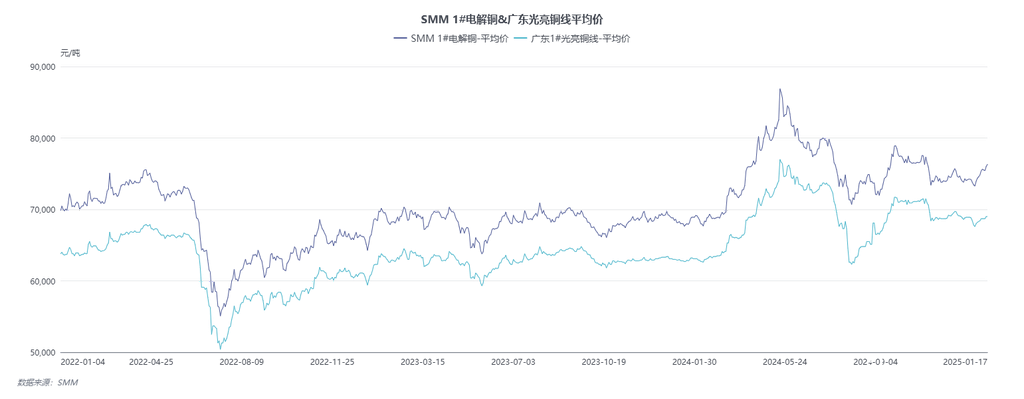

In 2024, copper prices experienced significant fluctuations, and the prices of secondary copper raw materials also showed a trend of rising first, then pulling back, followed by a slight rebound. In Q1, copper prices continued the stable trend of 2023. In Q2, due to tight overseas copper ore supply, sanctions on Russian copper and aluminum, and macro events such as US dollar copper boundary warehouses, copper prices surged to a historical high of 88,940 yuan/mt. However, as speculative sentiment faded, copper prices fell sharply in Q3. Starting in August, driven by market expectations of a US Fed interest rate cut, copper prices bottomed out. In Q4, on the eve of Trump's presidential election victory, copper prices showed wide fluctuations.

Since March 2024, domestic secondary copper raw material suppliers actively increased shipments due to rising copper prices to avoid risks from a pullback from highs. When copper prices climbed from 68,000 yuan/mt to 73,000 yuan/mt, the market had ample secondary copper raw material inventory, and even copper powder began to be favored by enterprises. Secondary copper rod enterprises increased inventory reserves to guard against further price increases. Although copper prices briefly pulled back and then climbed to a historical high of 88,940 yuan/mt, by mid-March, a large amount of secondary copper raw material inventory had been consumed. The high copper prices did not significantly boost trading volume, and the supply-demand relationship remained tight. Subsequently, copper prices fell sharply, and suppliers became more cautious, delaying shipments. Even though copper prices rebounded in H2, suppliers maintained a wait-and-see sentiment, and the annual supply of secondary copper raw materials remained tight.

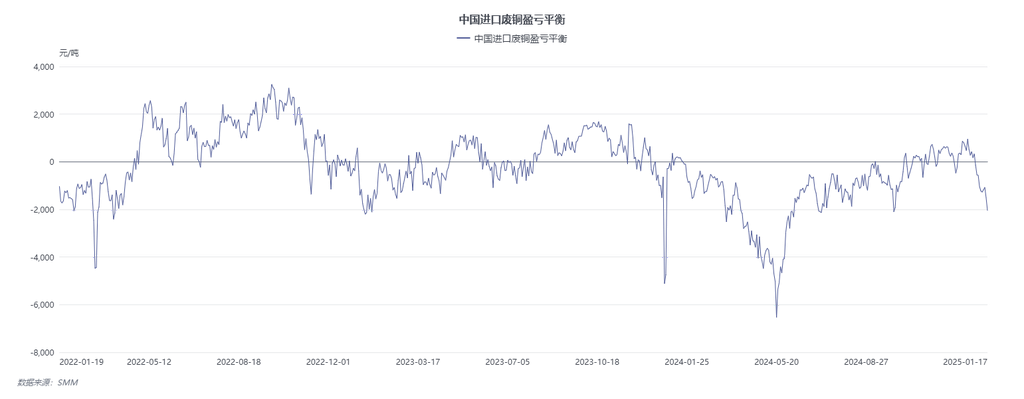

In 2024, the supply of secondary copper raw materials showed a trend of tightness at the beginning of the year, followed by easing. Early in the year, the rapid capacity expansion of domestic smelters in China led to a mismatch in copper ore supply, reversing the previous surplus situation. Concerns arose that domestic smelters might significantly reduce copper cathode production due to a lack of copper ore. Additionally, the closure of large overseas copper mines, bans on Russian copper deliveries in Europe and the US, and short squeezes by large traders drove copper prices significantly higher in H1. As copper prices rose, secondary copper raw material suppliers at home and abroad sold off large inventories, leading to a record high secondary copper raw material import volume of 180,900 mt (metal content) in April 2024. Subsequently, copper prices pulled back from highs, and the price difference between primary metal and scrap narrowed from 5,400 yuan/mt to 1,300 yuan/mt. Meanwhile, the Chinese government introduced "reverse invoicing" and the Fair Competition Review Regulations, significantly impacting the operating rates of scrap utilisation enterprises. Under the dual pressure of falling copper prices and weak demand, secondary copper raw material suppliers generally chose to hold back sales, leading to tighter supply in H2 and reduced circulation of low-priced secondary copper raw materials in the market. According to SMM estimates, the total supply of secondary copper raw materials in 2024 will reach 3.876 million mt (metal content), an increase of 327,000 mt compared to 3.549 million mt in 2023.

Since 2024, due to overseas demand for copper cathode exceeding supply, copper prices have shown a trend of "LME outperforms SHFE." Meanwhile, the US Fed's high-interest rate policy has kept the yuan under long-term pressure against the US dollar, resulting in a severe "inversion" in overseas secondary copper raw material prices. Despite this, domestic smelters showed stronger demand for secondary copper raw materials than in previous years. When prices were favorable, secondary copper raw material traders still opted to import. According to SMM estimates, the physical content of secondary copper raw material imports in 2024 is expected to reach 2.247 million mt, equivalent to 1.797 million mt in metal content, an increase of approximately 260,000 mt in physical content and 208,000 mt in metal content compared to the previous year.

In contrast, although the real estate sector performed poorly throughout the year despite multiple stimulus policies, the import volume of secondary brass ingots continued to decline. However, due to insufficient mineral resources for smelters, they had to import copper ingots from overseas, with the growth in imports exceeding the decline caused by secondary brass. According to SMM estimates, the metal content of imported secondary copper ingots in 2024 is expected to reach 482,200 mt, an increase of 92,900 mt compared to the same period last year.

Although the continuous depreciation of the yuan caused secondary copper raw material imports to remain unprofitable, the import window briefly opened from October to December, and import volumes still increased. This was mainly because the issue of tight copper concentrate supply remained unresolved, forcing smelters to rely on externally sourced anode plates to ensure copper cathode production. As a result, demand for secondary copper raw materials increased, and import traders were willing to increase imports only when they could secure certain profits through operations in domestic and overseas futures markets.

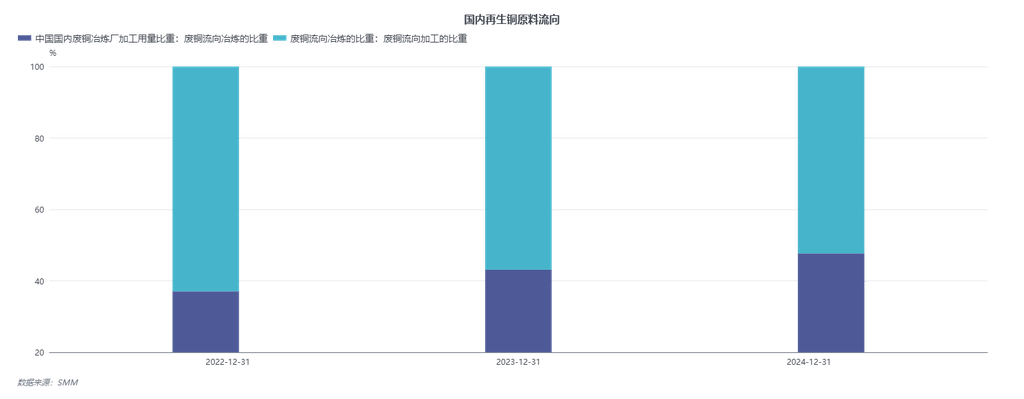

In 2024, tight copper ore supply significantly increased smelters' demand for anode plates. To ensure copper cathode production, smelters offered procurement prices for anode plates higher than the selling prices of secondary copper rods in the market. This prompted secondary copper rod plants to switch to producing anode plates. However, in H2, due to the implementation of new policies, many secondary copper rod plants suspended production to observe the situation, waiting for policy clarity before resuming operations. During this period, the secondary copper rod plants that continued production mainly focused on anode plates as their primary product, fulfilling long-term contracts with smelters. Consequently, the proportion of secondary copper raw materials flowing to the smelting sector increased significantly compared to previous years. According to SMM estimates, the proportion of secondary copper raw materials flowing to the smelting sector in 2024 is expected to reach 47.5%, while the proportion flowing to the processing sector will be 52.5% (compared to 43% and 57% in 2023, respectively).

In the processing sector, secondary copper rods remain the primary destination, followed by copper billets and copper foil. In April and July this year, new policies strengthened tax regulation on the circulation of secondary copper raw materials and standardized local government tax incentives and subsidies for secondary copper enterprises. These policies reduced the economic benefits of secondary copper raw materials due to tightened tax policies, compressing the profits of processing enterprises. Additionally, the new policies stipulated that newly added secondary copper rod capacity nationwide would no longer enjoy local preferential policies. As the economic benefits of scrap utilisation enterprises continued to decline, secondary copper rod plants may face capacity exit and consolidation in the future.

In the smelting sector, the high copper prices in Q2 gradually eased the supply of secondary copper raw materials. Against the backdrop of increased demand for anode plates from smelters, their profitability exceeded that of secondary copper rods, significantly driving secondary copper raw materials to flow into the smelting sector. According to SMM estimates, the volume of secondary copper raw materials flowing into the smelting sector in 2024 is expected to reach 1.84 million mt, an increase of approximately 330,000 mt compared to the previous year. Although secondary copper raw material supply tightened in H2 and new policies impacted the operating rates of secondary copper rod plants, the switch to anode plate production compensated for the raw material shortage caused by insufficient copper ore, ensuring copper cathode production.

In the future, the flow of secondary copper raw materials may undergo significant changes, with the ratio between the processing and smelting sectors potentially shifting from the current 6:4 to 4:6.

Looking ahead, the global secondary copper market is undergoing significant changes. Overseas, local secondary copper smelters in Europe and the US are gradually coming online, leading to more secondary copper raw materials being consumed in local markets. Additionally, accelerated urbanization in regions like India and Dubai is driving increased copper demand. Meanwhile, customs policies overseas are relatively more lenient compared to China. After Trump takes office in 2025, he may impose a 10% tariff on Chinese imports, while China imposed a 25% tariff on US secondary copper raw materials in 2018. Against this backdrop, many Chinese import traders have suspended secondary copper raw material purchases from the US since mid-to-late November, indicating that China's secondary copper imports may undergo adjustments due to superior policies in other countries and uncertainties in China-US trade relations.

Domestically, in 2024, China will implement trade-in subsidy policies for home appliances and NEVs, driving the scrapping of vehicles and appliances beyond 2023 levels. Over the next 15-20 years, recyclable secondary copper raw materials are expected to grow significantly. Additionally, the establishment of the China Resource Recycling Group in September 2024 provides strong support for promoting the recycling of secondary resources. With support from national policies, the group is expected to expand the coverage of domestic secondary resource recycling, promoting a full-chain "internal circulation" economy from initial recycling to end-use enterprises, accelerating the process of making domestic secondary copper raw materials a major supply source. Furthermore, in December, the State Council issued a notice to set up pilot programs for scrapped home appliance recycling in various cities, which will increase the recycling volume of old home appliances to some extent, thereby boosting domestic secondary copper raw material supply.

From 2024 to 2030, China's domestic secondary copper raw material supply is expected to increase from 2 million mt to 3.34 million mt. This will provide more raw material security for the domestic copper industry and enhance market competitiveness.